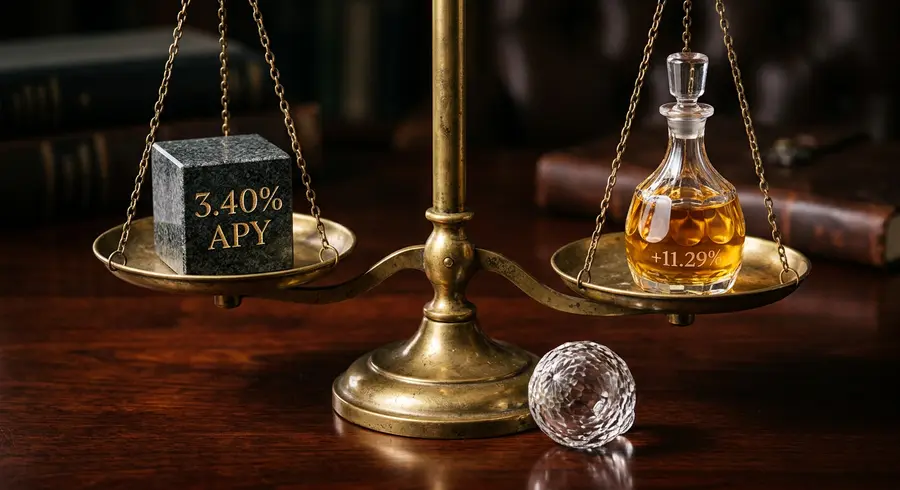

For high-income professionals, SCHD's 3.06% after-tax yield and +11.29% 3-year return significantly outperform Capital One 360's 2.14% after-tax yield, despite its zero-risk profile.

Marcus Sterling

Senior Financial Strategist

Specializing in premium banking optimization and wealth accumulation strategies. 15+ years advising high-net-worth individuals on maximizing financial instruments.

For sophisticated investors in 2025, the Capital One 360 Performance Savings account's 3.40% APY provides absolute principal protection but represents a significant opportunity cost. The Schwab U.S. Dividend Equity ETF (SCHD) delivers a superior 3-year annualized return of +11.29% and a 43% higher after-tax yield for high earners due to its qualified dividend structure. The Vanguard Real Estate ETF (VNQ) offers the highest current yield at 3.94% but is hampered by sector-specific headwinds and unfavorable tax treatment. The optimal strategy is not a singular choice but a calculated allocation across all three, weighted by an investor's time horizon and risk tolerance.

Yield, Cost, and Tax Structure Analysis

A direct comparison of yields is misleading without accounting for expense ratios and, most critically, tax treatment. Capital One's 3.40% APY is net of all costs but is fully exposed to ordinary income tax rates, which can erase over a third of the return for high-income professionals. In contrast, SCHD's minimal 0.06% expense ratio and qualified dividend treatment create a substantial after-tax advantage. While VNQ boasts the highest pre-tax yield, its REIT distributions are taxed as ordinary income, placing it on par with a savings account from a tax perspective but with significantly higher market risk.

Metric

Capital One 360

SCHD (Dividend ETF)

VNQ (REIT ETF)

Current Yield

3.40% APY

3.82% Dividend Yield

3.94% Dividend Yield

Expense Ratio

None

0.06%

0.13%

Net Yield (Pre-Tax)

3.40%

3.76%

3.81%

Tax Treatment

Ordinary Income

Qualified Dividends (15-20%)

Ordinary Income (Unqualified)

After-Tax Yield (37% Bracket)

2.14%

3.06%

2.48%

FDIC Insurance

Yes, up to $250,000

No

No

For an investor in the 37% federal tax bracket, SCHD's after-tax yield of 3.06% (3.82% × (1 - 0.20)) is decisively superior to Capital One 360's 2.14% (3.40% × (1 - 0.37)). This tax efficiency gap is a permanent structural advantage for qualified dividend ETFs within a taxable investment portfolio. VNQ's after-tax yield of 2.48% lands in the middle, offering a 34 basis point premium over the savings account but failing to match SCHD's tax-advantaged income stream.

Historical Performance vs. Guaranteed Returns

While cash provides stability, its long-term performance drag is substantial. Over the past three years, an investor holding funds in Capital One 360 would have missed significant growth, even accounting for market volatility. SCHD's +11.29% annualized three-year return demonstrates the power of compounding dividends and capital appreciation in a portfolio of fundamentally sound, large-cap U.S. companies. VNQ's performance has been more muted at +5.07% annualized over three years, largely due to a severe -26.25% drawdown in 2022 as interest rates rose, a key risk factor for the real estate sector. The 2024-2025 period saw equities face headwinds, with SCHD posting a -1.99% one-year total return. However, its dividend yield of 3.82% offset a significant portion of the capital loss, showcasing the income-cushioning effect of dividend strategies.

Capital One 360 Guaranteed Annual Return (Zero Volatility)

+11.29%

SCHD 3-Year Annualized Total Return (Including Dividends)

-7.89%

Annual Opportunity Cost of Cash vs. SCHD (3-Year Average)

The core trade-off is clear: accepting equity risk has historically compensated investors handsomely. A $50,000 investment in Capital One 360 three years ago would be worth approximately $55,200 today, with no fluctuation. The same $50,000 in SCHD, with dividends reinvested, would have grown to approximately $69,400, a surplus of over $14,000, despite experiencing periods of market decline. This quantifies the cost of safety for investors with a time horizon sufficient to absorb market cycles.

Risk Profiles and 2025 Market Outlook

Each instrument carries a distinct risk profile directly tied to the 2025 macroeconomic environment, particularly Federal Reserve policy. The consensus forecast for a Fed Funds rate settling in the 3.5-4.0% range presents different challenges and opportunities for each asset.

Capital One 360: Zero downside principal risk, FDIC-insured liquidity. Best for emergency funds and goals under 2 years.

SCHD: Proven long-term total return, qualified dividend tax benefits, and a dividend cushion during market drawdowns. Core holding for 5+ year horizons.

VNQ: Excellent inflation hedge through real estate values and rents. Provides non-correlated diversification to a traditional stock/bond portfolio.

Key Risks & Drawbacks

Capital One 360: Guaranteed loss of purchasing power against historical inflation. APY is subject to reduction if the Fed cuts rates.

SCHD: Subject to equity market drawdowns (Max historical: -33.37%). Underperforms growth-heavy indexes during bull markets.

VNQ: Extremely sensitive to interest rate hikes, which depress REIT valuations. Subject to sector-specific risks like commercial real estate vacancies.

For Capital One 360, a move by the Fed to cut rates would likely lead to a swift reduction in its APY, potentially toward the 3.0% level. For SCHD, a stable or slightly lower rate environment is supportive, as it reduces the discount rate on future earnings and makes its dividend yield more attractive relative to bonds. VNQ remains the most sensitive; it benefits most from aggressive rate cuts but faces significant valuation headwinds if rates remain elevated above 4.0%.

Tax-Loss Harvesting Alert for VNQ Holders

VNQ's -6.93% price return over the past year presents a strategic tax-loss harvesting opportunity. Investors can sell their position to realize a capital loss, which can offset gains elsewhere in their portfolio. To avoid the wash-sale rule, the position can be replaced with a similar but not "substantially identical" REIT ETF like XLRE or SCHH for 31 days before repurchasing VNQ.

Actionable Portfolio Allocation Frameworks

A blended approach tailored to risk tolerance provides the most robust solution. Below are three allocation models for a $50,000 portfolio, demonstrating the trade-offs between income generation, growth potential, and downside protection. The analysis includes a stress test simulating a -25% equity market drawdown to quantify potential portfolio declines.

Conservative Allocation (50% C1 / 30% SCHD / 20% VNQ): Generates $1,817 in annual income (3.63% blended yield). In a severe downturn, the maximum expected portfolio drawdown is limited to approximately 5.3%. This is ideal for investors within 5 years of retirement or those with low risk tolerance.

Moderate Allocation (30% C1 / 35% SCHD / 35% VNQ): Produces $1,868 annually (3.74% blended yield). This balanced approach increases exposure to equity growth while the 30% cash holding mitigates volatility, limiting a stress-test drawdown to 8.3%. Suitable for investors with a 5-10 year horizon.

Aggressive Allocation (10% C1 / 45% SCHD / 45% VNQ): Maximizes income and growth potential, yielding $1,916 per year (3.83% blended yield). This allocation accepts higher risk for higher reward, with a potential maximum drawdown of 10.8%. It is designed for investors with a 10+ year time horizon who prioritize total return.

Capital One 360 Performance Savings: The Sophisticated Investor's Guide

What is Capital One's current APY in 2025 and how does it compare to competitors?

Capital One 360 Performance Savings offers 3.40–3.50% APY as of November 2025, approximately 8–9 times the national average of 0.40%. While competitive among traditional banks, premium online institutions like Varo Money (5.00% APY), Axos Bank (4.51%), and Newtek Bank (4.35%) offer higher yields, though often with withdrawal restrictions or balance requirements.

Are there any fees or minimum balance requirements for Capital One's high-yield savings?

No. Capital One 360 Performance Savings charges zero monthly maintenance fees, has no minimum opening deposit, and no minimum balance to earn the stated APY. Interest compounds monthly on all balances, regardless of size.

What are the eligibility requirements to open a Capital One 360 Performance Savings account?

You must be 18+ years old with a U.S.-based mobile phone number and either a valid Social Security Number or Individual Taxpayer Identification Number (ITIN). You'll need your name, date of birth, address, email, phone, employment information, annual income, and citizenship details. Account approval requires verification by Capital One, and you have 60 days to fund the account after approval.

Is Capital One safe and trustworthy for depositing savings?

Capital One holds an A+ BBB rating and maintains FDIC insurance up to $250,000 per depositor. The bank encrypts data, provides fraud protection with rapid card locking capabilities, and offers two-factor authentication. However, Trustpilot reviews reflect mixed customer service experiences, with some complaints about dispute handling and payment processing—typical concerns for any large financial institution.

What is the status of the Capital One $425M settlement as of November 2025?

On November 22, 2025, a federal judge rejected the $425 million settlement, ruling it inadequate compensation (covering less than 10% of lost interest). The original settlement targeted 360 Savings account holders (September 2019–June 2025) who allegedly lost over $2 billion in interest due to artificially suppressed rates. A revised settlement or trial is anticipated, with payments likely delayed until mid-2026.

Who is eligible for the Capital One settlement payout?

Customers who held a Capital One 360 Savings account (not 360 Performance) between September 18, 2019, and June 16, 2025, are eligible. Those who closed accounts by October 2, 2025, were entitled to ~15% larger payouts. Pending the judge's approval of a revised settlement, eligibility criteria may be reconsidered.

Capital One vs. Chase: Which savings account is worth it?

Capital One 360 Performance Savings (3.40% APY) significantly outperforms Chase Savings (0.01% APY). On $10,000, Capital One generates $340 annually versus $1 with Chase—a $339 advantage. Capital One offers no fees or minimums, while Chase waives its $5 fee only with $300+ daily balance maintenance.

Is Capital One High-Yield Savings a good idea compared to money market accounts or CDs?

For liquidity, Capital One 360 Performance Savings (3.40% APY) offers immediate access without withdrawal penalties. Capital One 360 CDs range 3.50–4.05% APY (6 months–5 years) but lock funds. Money market accounts typically earn 3.80–4.20% but may have balance minimums. Choose CDs for rate certainty; high-yield savings for flexibility; money market accounts for hybrid access.

What are the tax implications of earning interest on Capital One savings?

Capital One interest is taxed as ordinary income at your marginal federal tax rate. The bank issues Form 1099-INT by January 31 each year for all interest earned. There are no special tax breaks for high-yield savings accounts. On $10,000 at 3.40% APY ($340 annual interest), a 24% tax bracket investor owes ~$82 in federal taxes, reducing net return to ~2.58% after-tax APY.

How do I calculate my after-tax return on Capital One 360 Performance Savings?

Multiply the APY by (1 minus your marginal tax rate). At 3.40% APY and a 37% tax bracket: 3.40% × (1 – 0.37) = 2.14% after-tax APY. For a $50,000 deposit: $50,000 × 0.0214 = $1,070 net annual income after federal taxes (excluding state taxes and the 3.8% Net Investment Income Tax for high-income earners).

Which bank offers 7% interest on savings accounts in 2025?

In the U.S., no mainstream bank currently offers 7% on unlimited-balance savings accounts. The highest U.S. rates are ~5.00% (Varo Money). In the UK, First Direct and Zopa offer 7% on regular savers (limited monthly deposits of £250–£300), and Nationwide's Flex Regular Saver briefly offered 8% in 2023–2024 but has since dropped to 6.5%.

Can I earn 9% on my savings account in 2025?

No U.S. FDIC-insured savings accounts currently offer 9% APY. The highest verified rate is 5.00% from Varo Money. Historically, 9%+ rates appear only in high-risk cryptocurrency accounts, peer-to-peer lending platforms, or uninsured investments—not appropriate for emergency savings due to credit and volatility risks.

What was Nationwide's 8% savings account, and is it still available?

Nationwide (UK) launched its Flex Regular Saver at 8% in September 2023, the highest rate in a decade. It was limited to £200/month deposits and available only to current account holders. The account matured in 2024 and was replaced with a 6.5% variable rate. The 8% promotional rate is no longer available; current best UK rates for regular savers are 7% (First Direct, fixed).

Where can I get 5% interest on a savings account in 2025?

Varo Money offers up to 5.00% APY on the first $5,000 of deposits (with eligible direct deposit) and 2.50% on balances above $5,000. Other competitive rates include Axos Bank (4.51%), EverBank (4.30%), and UFB Direct (4.01%)—all with zero fees and no minimum balances. Rates fluctuate; confirm current APY before opening.

Should I move my savings from Capital One to a higher-rate bank?

It depends on your priorities. Capital One's 3.40% APY lags top competitors by ~1.5–1.7 percentage points. On $50,000, switching to Varo Money (5.00%) adds ~$800 annually before taxes. However, Capital One offers 200+ U.S. branches, strong mobile tools, and brand stability. If rate maximization is paramount and you don't need branch access, a switch to higher-yielding online banks warrants consideration. Monitor Capital One's rate quarterly for competitive shifts.

What is Capital One's interest compounding frequency and how does it affect earnings?

Capital One compounds interest monthly and credits it to your account monthly. On $10,000 at 3.40% annual APY compounded monthly, the effective APY is slightly higher (~3.41%) than simple annual interest due to monthly compounding. Using compound interest formula: $10,000 × [(1 + 0.034/12)^12 – 1] = $345.66 annual earnings, demonstrating minimal compounding benefit versus daily-compounding competitors.