Lifestyle Optimization

Premium Lifestyle Strategy for $200K Earners in 2025

July 31, 2025 · 6 min read

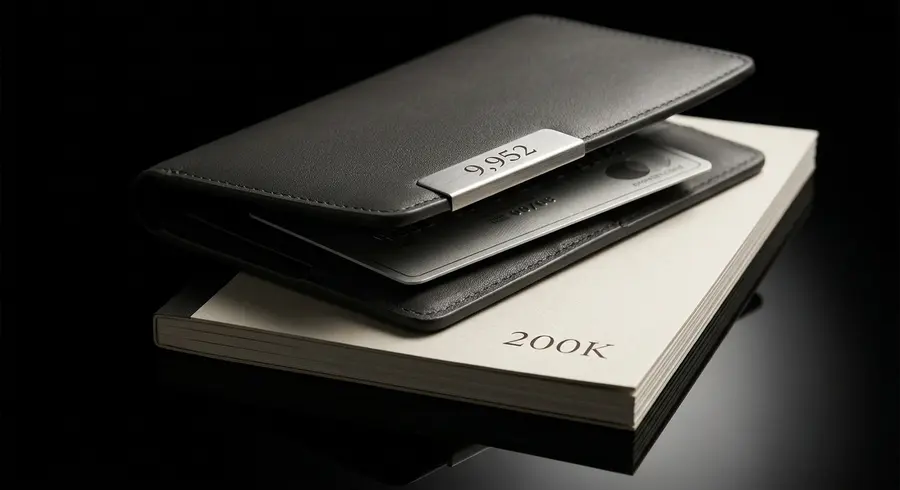

For a $200K earner, strategic tax-advantaged contributions generate $9,952 in annual savings—enough to fully subsidize the $895 Amex Platinum fee and unlock over $7,000 in first-year travel perks.

For a US household earning $200,000, optimizing tax-advantaged accounts generates $9,952 in annual tax savings, creating a direct subsidy for premium lifestyle perks. This strategy fully covers the annual fees of top-tier travel cards like the American Express Platinum, whose $7,200 in first-year benefits are unlocked using pre-tax dollars. The primary challenge for this income level is navigating Roth IRA contribution limits, making the Backdoor Roth strategy non-negotiable for tax-free growth. This approach is most effective for disciplined professionals who can systematically max out contributions and align spending with high-value credit card categories.

Tax Optimization: The $9,952 Annual Lifestyle Subsidy

The foundation of this strategy is not increased spending, but a reduction in tax liability. By systematically funding every available tax-advantaged account, a single US filer earning $200,000 can lower their effective tax rate from 25.39% to 20.41%. This reduction translates into tangible cash flow that can be reallocated to lifestyle enhancements. The total annual tax savings of $9,952 is derived from contributions that reduce taxable income at the earner's highest marginal tax bracket (32% for 2025).

$7,520

Annual tax savings from maxing out a $23,500 401(k) contribution in the 32% bracket.

$2,432

Combined tax savings from fully funding Health Savings ($4,300) and Flexible Spending ($3,300) accounts.

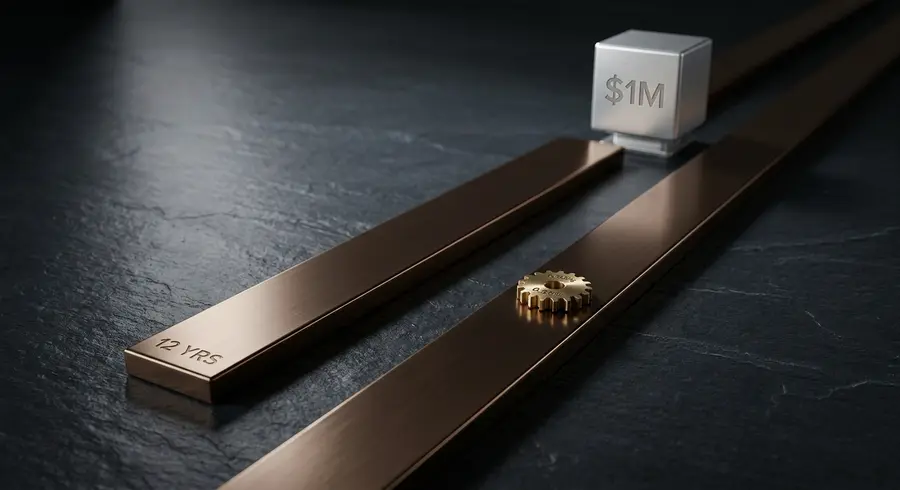

$1.7M

Projected 40-year tax-free growth of a Backdoor Roth IRA with $7,000 annual contributions at 7% growth.

For a UK-based professional earning £120,000, the opportunities are even more substantial. The UK tax system allows for a combined £24,000 in annual contributions to tax-advantaged accounts. This includes a £20,000 Stocks & Shares ISA, which provides tax-free growth on all dividends and capital gains, and a £4,000 Lifetime ISA (for ages 18-39) that comes with an automatic 25% government bonus, representing an immediate £1,000 gain plus tax-free growth. These contributions directly shield investment returns from the standard 20% capital gains tax.

-

US Contribution Breakdown (2025): A total of $38,100 is deferred into tax-advantaged accounts: $23,500 (401k), $7,000 (Backdoor Roth IRA), $4,300 (HSA), and $3,300 (FSA).

-

UK Contribution Breakdown (2025/26): A total of £24,000 can be invested tax-efficiently via ISAs, shielding significant growth from income and capital gains taxes.

-

Dual Residency Strategy: For individuals with income in both jurisdictions, the Foreign Tax Credit (FTC) is essential. By filing Form 1116, UK taxes paid can be credited against US tax liability, preventing double taxation on the same income.

The Backdoor Roth IRA: A Mandatory Strategy for $200K Earners

At a $200,000 income, direct contributions to a Roth IRA are prohibited, as the phase-out for single filers ends at $165,000 in 2025. The required workaround is the Backdoor Roth IRA. This two-step legal process involves making a non-deductible contribution to a Traditional IRA and immediately converting it to a Roth IRA. The success of this strategy hinges entirely on avoiding the IRS pro-rata rule, a common and costly mistake.

See also: Financial Independence Roadmap for High Earners

The pro-rata rule requires that any Roth conversion be taxed based on the proportion of pre-tax and after-tax money held across all of an individual's IRA accounts (Traditional, SEP, SIMPLE). If an individual has a pre-existing $93,000 rollover IRA and contributes a new $7,000 for conversion, the IRS considers 93% of the conversion to be taxable, defeating the purpose of the strategy.

Critical Pro-Rata Rule Violation Warning

You must have a $0 balance in all pre-tax IRAs (Traditional, SEP, SIMPLE) on December 31 of the conversion year. The solution is to roll any existing IRA balances into your current employer's 401(k) plan before executing the Backdoor Roth conversion. This action removes those assets from the pro-rata calculation, making the conversion of your new non-deductible contribution 100% tax-free.

2025 Premium Credit Card Value Analysis

With tax savings generating over $9,900 in discretionary funds, the high annual fees of premium travel cards are fully subsidized. The American Express Platinum, despite its increased $895 fee, delivers the highest net value. Its comprehensive statement credits and unparalleled lounge access offer a total first-year benefit package valued at $7,200, resulting in a net gain of $6,305. This represents a 704.5% return on the annual fee. The Chase Sapphire Reserve is a strong alternative, particularly for those who prioritize dining rewards and direct travel booking flexibility.

Related: US vs UK: Building a $2.3M Fortune on an Average Salary

| Card (2025) | Annual Fee | Welcome Bonus Value | Annual Credits | Net Year 1 Value | Ongoing Net Value (Yr 2+) |

| Amex Platinum | $895 | $2,250 | $3,500+ | $6,305 | $4,055 |

| Chase Sapphire Reserve | $795 | $1,875 | $2,700+ | $5,180 | $3,305 |

| Capital One Venture X | $395 | $1,500 | $400 | $2,105 | $605 |

| Citi Prestige | $495 | $750 | $600 | $1,655 | $905 |

The Amex Platinum's value is heavily weighted towards its extensive list of statement credits, which now exceed $3,500 annually. These include credits for Uber, digital entertainment subscriptions (Disney+, NYT, Peacock), hotel bookings, dining via Resy, and airline incidentals. Its primary advantage remains the Global Lounge Collection, offering access to Centurion Lounges, Priority Pass, and Delta Sky Clubs—a value estimated at $850 per year for a frequent traveler.

Q1 2025 Implementation Blueprint

Achieving this level of optimization requires front-loading key financial decisions into the first quarter of the year. This timeline provides a week-by-week action plan to establish the tax-advantaged accounts and secure the credit card benefits that fuel the strategy.

See also: Building Generational Wealth: US vs. UK Strategy Guide

1

Week 1 (Jan 1-7): Tax-Advantaged Account Setup

Adjust payroll deductions to max 401(k) contributions ($23,500/yr). Enroll in and schedule funding for your HSA ($4,300) and FSA ($3,300). This must be done during your employer's open enrollment period.

2

Week 2 (Jan 8-14): Execute Backdoor Roth IRA

Confirm a $0 balance in all other Traditional/SEP/SIMPLE IRAs. Open a new Traditional IRA, deposit a $7,000 non-deductible contribution, and execute the conversion to a Roth IRA within 1-2 business days.

3

Week 3 (Jan 15-21): Apply for Premium Credit Card

Apply for the American Express Platinum or Chase Sapphire Reserve. Upon approval, note the minimum spend requirement and deadline to earn the welcome bonus (typically ~$6,000 in 3 months).

4

Weeks 4-12 (Jan 22-Mar 31): Activate and Optimize

Meet the minimum spend requirement on your new card to secure the welcome bonus points (~$2,250 value). Systematically activate all available statement credits (e.g., airline fee, Uber cash, hotel credit) to begin extracting value immediately.

By following this blueprint, a household can implement the entire financial strategy within 90 days. Over a five-year period, the combined value from tax savings ($49,760) and net credit card benefits ($20,775 with Amex Platinum) totals $70,535. This represents a significant injection of value, transforming a high income into a strategically funded premium lifestyle without requiring additional out-of-pocket expenditure.

The Premium Lifestyle Playbook: Maximizing Wealth on an Upper-Middle-Class Income

What is the upper-middle-class income threshold in 2025?

Upper-middle-class households in the US earn between $117,000-$150,000 annually, according to 2025 Pew Research Center analysis. In 2025 tax brackets, this typically falls within the 24% marginal tax bracket for single filers ($105,701-$201,775) and 22-24% for married couples filing jointly ($211,401-$403,550).

What is the best rewards credit card for upper-middle-class professionals in 2025?

The Amex Platinum Card ($895 annual fee) offers $3,500+ in annual value through $400 Resy dining credits, $300 lululemon credit, $120 Uber One, $200 Oura Ring credit, plus 5X points on flights/prepaid hotels. Chase Sapphire Reserve ($795 fee) delivers $2,700+ value with $300 travel credit, $300 annual dining statement credits, and 8X points on Chase Travel purchases.

Is the Amex Platinum Card worth it at $895 annually for affluent professionals?

Yes, if you fully utilize benefits: frequent travelers break even with just hotel credits + dining benefits at $600+$400=$1,000 in credits alone. 2025 analysis shows 127% ROI for active users combining travel, dining, entertainment subscriptions, and airport lounge access. However, non-travelers should consider mid-tier cards with $95-$395 annual fees instead.

What is the most generous rewards program globally in 2025?

Air France-KLM's Flying Blue was voted world's best airline rewards program for 2025, offering 40+ airline transfer partners, flexible award pricing, family pooling, and ecosystem-wide flexibility. American Express Membership Rewards ranks highest for lifestyle integration, offering transfers to 18+ travel partners plus shopping, dining, and entertainment flexibility.

Which fast food restaurant has the best rewards app in 2025?

Wendy's leads with 27 reward redemption options, three pickup methods (drive-thru, walk-in, delivery), and earning points on every dollar spent. McDonald's excels for exclusive promotions with daily app-only deals redeemable in-store. Starbucks ranks best for engagement with bonus star challenges and real-time order tracking.

What restaurants give free food when you download their app in 2025?

Major chains offering welcome app incentives include: McDonald's (FREE Big Mac with $1+ purchase), Taco Bell (FREE Crispy Taco), Wendy's (200 bonus points + deals), Chipotle (FREE Guacamole with $5+ purchase), IHOP (FREE 5-pancake stack), Starbucks (FREE drink with first $5 purchase), Panera (FREE pastry + 30 days free delivery), and Red Lobster (12 FREE Cheddar Bay Biscuits with $15+ to-go order).

What is the 30/30/30 rule for restaurants?

The 30/30/30/10 rule allocates restaurant revenue as: 30% food costs, 30% labor costs, 30% operating expenses (rent, utilities, insurance), leaving 10% profit margin. This benchmark helps restaurant owners and diners understand cost structure—relevant when evaluating restaurant loyalty program value and menu pricing.

What is loyalty in 2025 for premium consumers?

2025 loyalty emphasizes personalization, emotional connection, and experience over transactional rewards. Top programs like Amex Membership Rewards, Starbucks Gold, and Sephora Rouge combine tiered status, exclusive experiences (wine tastings, early access), gamification elements, and data-driven personalization. 82% of customers report greater loyalty to brands creating emotional connections, with experience-driven rewards increasing revenue 5%+.

Which restaurant has the best rewards program in 2025?

Starbucks Rewards leads with 3X visit frequency from non-members, 3X higher spending, and tiered status (Green/Gold). Members earn stars redeemable for $0.25-$4 value items, plus birthday rewards, free refills, and gamified challenges. Panera MyPanera personalizes rewards by member preference as of October 2025, offering selectable free items rather than one-size-fits-all benefits.

What is the most successful rewards program of 2025?

Amazon Prime remains the world's most successful paid loyalty program ($139 annual fee), blending retail discounts, free 2-day shipping, Prime Video, and ecosystem benefits—generating 55%+ program value through non-shopping categories alone. Marriott Bonvoy and Hilton Honors dominate travel with flexible redemptions across 40+ hotel partners and dynamic pricing models.

What lifestyle budget should upper-middle-class earners allocate monthly?

On $117K-$150K annual income (~$9,750-$12,500 monthly), financial experts recommend: 50% essential expenses (housing, insurance, debt), 30% lifestyle/discretionary, 20% savings/investments. This allows $2,925-$3,750 monthly for premium experiences—sufficient for upscale dining ($800-$1,200/month with rewards), luxury subscriptions ($200-$300), and travel ($1,000-$1,500/month during quarter).

How can upper-middle-class earners maximize credit card ROI in 2025?

Stack cards strategically: use premium cards ($795-$895) for travel/dining/subscriptions where credits apply, redirect everyday spending to 2-5% cashback cards (Wells Fargo Active Cash 2%, Chase Freedom Flex 5% rotating). Target minimum $250K annual spending to justify premium card fees. Example: $50K annual travel + dining spend on Sapphire Reserve = $2,700 value vs. $795 fee = $1,905 net benefit.

What tax-advantaged strategies build wealth for upper-middle-class professionals?

2025 strategy: max out 401(k) contributions ($23,500 limit), add Roth IRA ($7,000 limit), establish HSA if eligible ($4,150 individual/$8,300 family, triple tax-free). Wealth builders at this income maintain 15-20% savings rates across these accounts, targeting 10-year doubling via compound growth. Defer income through deferred comp/SEP-IRA if self-employed, staying under 24% tax bracket threshold (~$197,300 for single filers).

What store has the best rewards program in 2025?

Sephora Beauty Insider dominates retail with tiered rewards (Insider free/VIB $350+/Rouge $1,000+ annual spend) offering birthday gifts, free beauty classes, 2-3X event multipliers, and exclusive product access. Target Circle (free) and Amazon Prime (paid) rank highly for omnichannel integration. Luxury retailers like LVMH offer exclusive VIP programs with personal shoppers and early access, though benefits vest at $10,000+ annual spend.

How should upper-middle-class earners structure their investment portfolio in 2025?

Diversify across: S&P 500/Nasdaq index funds (40%), dividend stocks (15%), REITs (10%), high-yield savings (8-9% APY for emergency fund), real estate (20-25% equity), and business/side income (10-15%). This 15-20% savings rate at upper-middle income generates $17,550-$23,400 annually invested—compounding to $500K+ over 20 years at 7% real returns. Prioritize tax-advantaged accounts first.

What are the best lifestyle rewards in 2025?

Top 2025 lifestyle rewards include: Amex Platinum ($3,500+ annual value in credits + lounge access), Chase Sapphire Reserve ($2,700+ dining/travel/entertainment credits), airline programs with upgrade certificates, hotel elite status with complimentary upgrades/breakfast, and subscription services (Apple Music, ESPN+, Disney+). Experience-driven programs (exclusive events, wine tastings, chef tables) show 5%+ revenue lift for premium brands.